Things could get interesting

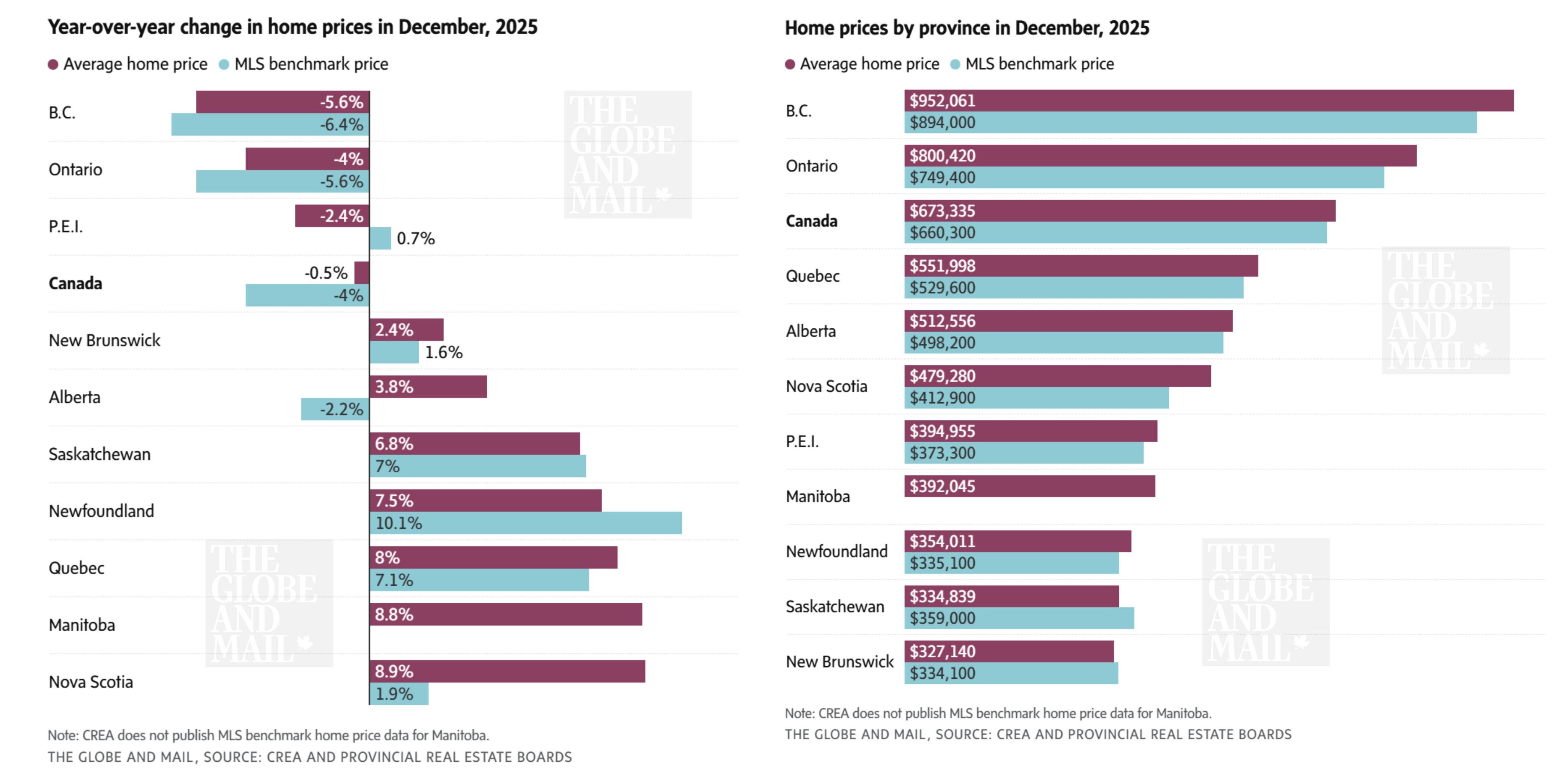

January was a rough way to open the year for Metro Vancouver real estate. Home sales fell 29 percent year over year and landed roughly 35 percent below the ten year average. January seems to be a continuation of a trend that has been building for several years and quietly intensified in 2025.

On paper, this market should be moving. Interest rates are down from their peak. Prices have corrected meaningfully from 2022 highs. Inventory is no longer scarce. Developers are offering incentives that would have been unthinkable a few years ago. And yet buyers remain largely on the sidelines.

The problem is not affordability alone. It’s confidence. Across Vancouver, buyers are struggling to reconcile conflicting signals. They see prices off their highs but still historically expensive. They see rate cuts, but not a return to cheap money. They see incentives, but also read headlines about stalled projects, receiverships, and policy uncertainty. The result is paralysis.

As Eric Carlson, CEO of Anthem Properites put it recently, “buyers are not saying no. They are saying maybe. They qualify. They like the product. They understand the location. Then, when it comes time to write a contract, they hesitate. A week turns into two. Conversations go quiet. The conversion from interest to commitment is where the market is breaking down.”

This hesitation defined the presale market in 2025. By almost every metric, last year was one of the weakest presale years in more than 3 decades. Launches were scarce. Unit releases were limited. Absorption rates hovered around 30 percent. What little activity did occur was concentrated in low rise and townhouse product, mostly outside the City of Vancouver. High rise urban presales were largely absent.

That matters, because Vancouver’s development pipeline depends on presales to function. Most projects require 60 to 80 percent presales to secure financing. When buyers step back, launches stop. When launches stop, future supply shrinks. The effects are delayed, but they are real.

At the same time, investors have largely disappeared. For years, investor purchasers were a meaningful component of the presale market, especially in Vancouver’s urban core. That demand has evaporated, and for rational reasons. Rents are no longer rising. Short term rentals have been curtailed. Financing costs increased faster than achievable returns. Many investors are already underwater on existing holdings and are in no position to add more leverage.

Just as importantly, investors now have alternatives. Equity markets have performed well. Cash yields are no longer negligible, and Gold and Silver outperformed almost everything. In an environment defined by uncertainty, it is easier to sit on the sidelines with liquidity than to commit to a multi year presale with unclear exit economics.

Developers, for their part, are adapting. Pricing has adjusted. Incentives have become normalized. Finished inventory is being actively marketed rather than quietly held back. In practical terms, buyers today have more choice and more leverage than they have had in years. This is not a crash environment, but it is no longer a sellers market either.

Some developers describe the current phase as a move toward calmness. Not growth, not exuberance, but stability. Sustained mediocrity, as unglamorous as that sounds, is easier to plan around than volatility. For buyers, that kind of environment often looks far more attractive in hindsight than it feels in the moment.

As I have mentioned before, how Canada measures housing starts is... odd. And it's harming our ability to understand what's going on with new housing construction and demand. Housing starts are not counted until the home is built back to grade, which can be as much as 2 years later since a housing start has officially started. If housing starts were on the rise in 2025, get ready for them to fall off a cliff over the next few years. By 2027, we will start to see meaningful recovery due to supply constraints, and by 2028 it may be time to buckle up as housing starts, as they are recorded now will be almost non-existent, and with no new supply coming to the market, prices are sure to start rising.

Population dynamics complicate the picture. Immigration has been a major driver of housing demand over the past decade, particularly in rental markets. Recent policy shifts are changing that trajectory. International student arrivals have fallen sharply. Temporary resident growth has slowed. Overall immigration targets have been revised downward.

In Vancouver, the impact is already visible. Vacancy has increased modestly. Rents have softened. The assumption that any unit will automatically rent at a rising rate no longer holds. That shift directly affects investor demand and indirectly influences buyer psychology.

At the same time, it is still unclear how many temporary residents will ultimately leave, how many will stay, and how quickly population growth resumes. Businesses, lenders, and buyers all struggle when outcomes are difficult to model. Uncertainty itself becomes a headwind.

Layered on top of this is policy friction. The mortgage stress test remains in place, limiting purchasing power even as prices adjust. Trade tensions, political turnover, and legal questions around land ownership add noise, even if their direct housing impact is limited. For many households, this accumulation of uncertainty makes waiting feel safer than acting.

Finally, there is the issue of competing inventory. Projects launched years ago are completing into a softer market. Unsold finished units are now competing with resale listings and future presales. From a buyer’s perspective, this is a rare window of optionality. From a developer’s perspective, it is a clearing process that needs to occur before new launches can meaningfully resume.

All of this explains why the Vancouver market feels slow without feeling broken. Demand has not disappeared. It has become cautious. Buyers are not priced out so much as unconvinced. They are waiting for clarity, not perfection.

History suggests that these periods tend to look like missed opportunities in retrospect. The challenge is that they never feel that way while you are living through them.

Vancouver real estate is not frozen. It is hesitating. And hesitation, in markets like this, rarely lasts forever.